English

English

Office Clearance for SMEs: Affordable Solutions Businesses

Office Clearance for SMEs: Affordable Solutions Businesses

P2P Lending for Small Businesses: A Growing Financial Solution

P2P Lending for Small Businesses: A Growing Financial Solution

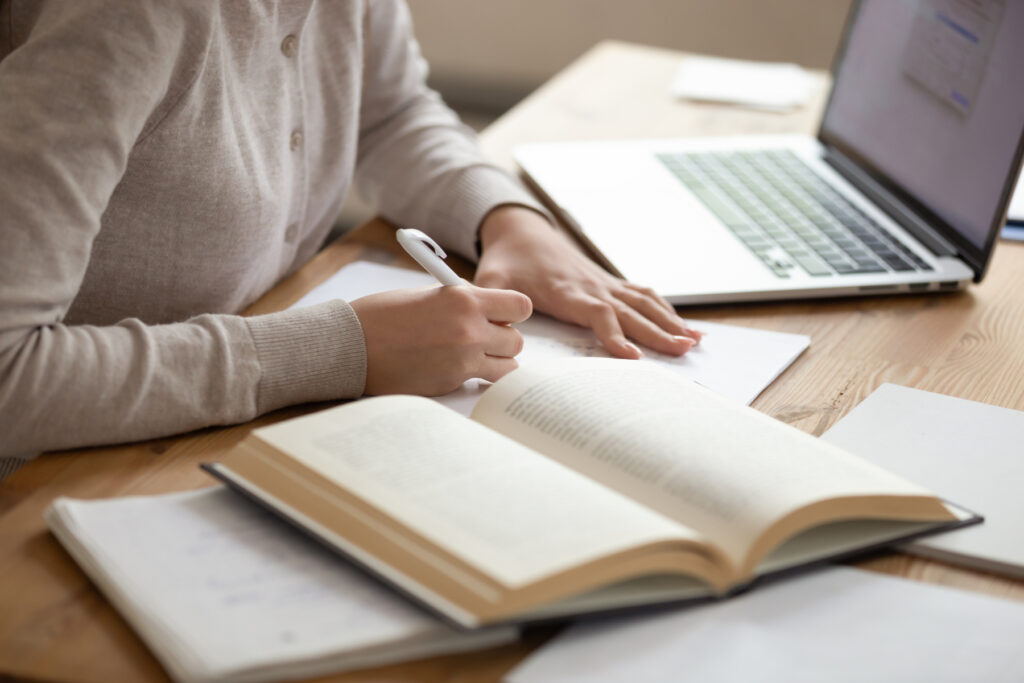

Small businesses have always been the backbone of the economy, creating jobs, driving innovation, and offering a wide range of goods and services. However, one of the biggest hurdles small businesses face is access to financing. Traditional banks often have strict lending requirements, making it difficult for small business owners, especially those from underserved communities, to secure loans. This is where Peer-to-Peer (P2P) lending comes in—a rapidly growing financial solution that is transforming the way small businesses can access funds.

P2P lending is a method of borrowing and lending money that connects individual lenders directly to borrowers through an online platform. Instead of going through a traditional financial institution like a bank, small business owners can now receive loans from private investors who are willing to lend their money at competitive interest rates. In this blog, we’ll explore how P2P lending is benefiting small businesses and the role of key licenses like P2P License, Payment Bank License (RBI), and Prepaid Payment Instrument License in the growth of this innovative lending model.

Why P2P Lending is Ideal for Small Businesses

Access to Quick Funds

One of the biggest advantages of P2P lending is that it allows small businesses to access funds quickly. Traditional loan application processes often involve lengthy paperwork, approval times, and rigorous checks. In contrast, P2P platforms streamline the entire process, enabling small businesses to receive loans much faster—often within a few days or weeks. This is particularly helpful for businesses that need funds to cover urgent expenses such as inventory restocking or emergency repairs.

Lower Interest Rates

Since P2P lending platforms directly connect borrowers with individual lenders, there are fewer intermediaries involved. This often results in lower interest rates for small business owners compared to traditional banks. With reduced overhead costs and less administrative bureaucracy, P2P platforms can offer more competitive rates that make loans more affordable.

Flexible Loan Terms

Unlike traditional banks, which may offer rigid loan terms, P2P lending platforms typically offer more flexibility in terms of repayment schedules, loan amounts, and the types of loans available. Small business owners can find loan terms that better suit their specific financial needs, whether it’s a short-term loan to cover cash flow gaps or a long-term loan for expansion.

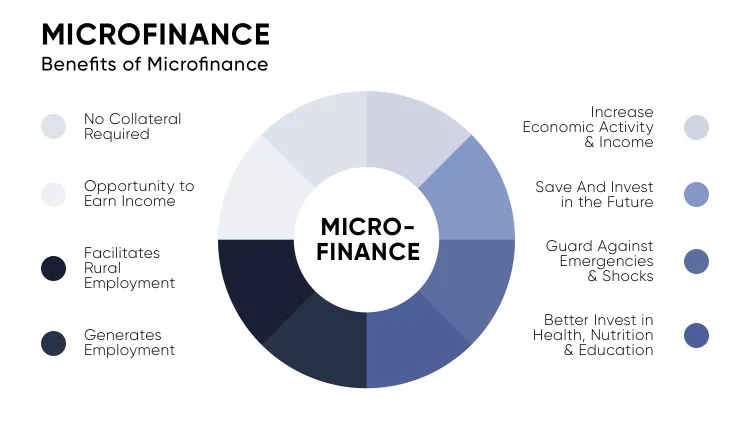

Financial Inclusion

P2P lending plays a crucial role in promoting financial inclusion. Many small businesses, especially those in rural areas or from underbanked communities, struggle to access financing from traditional institutions due to a lack of credit history or collateral. P2P platforms, however, are often more willing to lend based on factors beyond traditional credit scores, such as the business’s growth potential and cash flow.

Read more: https://onlinetechlearner.com/regulatory-changes-for-nbfcs-whats-new-in-2025/

Key Licenses Enabling P2P Lending Growth

For P2P lending to function legally and securely, platforms must adhere to regulatory frameworks set by governing bodies like the Reserve Bank of India (RBI) and other financial regulators. Here are some important licenses that play a role in the growth of P2P lending platforms in India:

P2P License

In India, the P2P License is issued by the Reserve Bank of India (RBI). This license ensures that P2P lending platforms operate under a structured and regulated framework. The P2P license mandates that platforms adhere to certain operational standards, such as maintaining appropriate risk management practices, having an effective grievance redressal system, and keeping customer data secure. For small business owners, choosing a P2P platform with the appropriate license adds a layer of security, ensuring that their loan application and repayment process is backed by regulatory standards.

Payment Bank License (RBI)

A Payment Bank License issued by the RBI allows institutions to provide a wide range of payment services, including the ability to accept deposits, offer payment services, and facilitate money transfers. While not every P2P lending platform requires a Payment Bank License, some platforms may partner with payment banks to process loan repayments or disburse funds. The presence of a licensed payment bank further ensures that the financial transactions involved in P2P lending are secure and compliant with RBI regulations, benefiting both borrowers and lenders.

Prepaid Payment Instrument License

The Prepaid Payment Instrument License (PPI License) is granted by the RBI to entities that provide prepaid payment instruments, such as digital wallets. Some P2P platforms use PPIs to facilitate loan disbursements or repayments. For instance, if a small business borrows funds via a P2P platform, the funds may be disbursed into a prepaid digital wallet, which can then be used to make payments or transferred to a business account. The PPI license ensures that these transactions are safe, transparent, and regulated.

The Future of P2P Lending for Small Businesses

The rise of P2P lending has opened up new opportunities for small businesses, especially those that have traditionally struggled to access funding. With the growing adoption of digital platforms, the increasing number of microfinance company registrations, and the expanding range of licenses like the P2P License and Prepaid Payment Instrument License, the future of P2P lending looks promising.

As technology continues to advance, we can expect P2P platforms to offer even more innovative solutions, such as AI-driven credit scoring, blockchain-based lending, and instant loan disbursements. Small businesses will benefit from these innovations, gaining access to more affordable and flexible financing options that support their growth and sustainability.

Conclusion

P2P lending is rapidly emerging as a valuable financial solution for small businesses. It provides quick access to funds, lower interest rates, and flexible loan terms that traditional banking institutions often cannot offer. By leveraging key licenses such as the P2P License, Payment Bank License (RBI), and Prepaid Payment Instrument License, P2P lending platforms are able to operate securely and comply with regulatory standards, offering a safe and reliable alternative for business owners. As the P2P lending landscape continues to evolve, small businesses are set to benefit from an even more accessible and dynamic financial ecosystem.