English

English

Office Clearance for SMEs: Affordable Solutions Businesses

Office Clearance for SMEs: Affordable Solutions Businesses

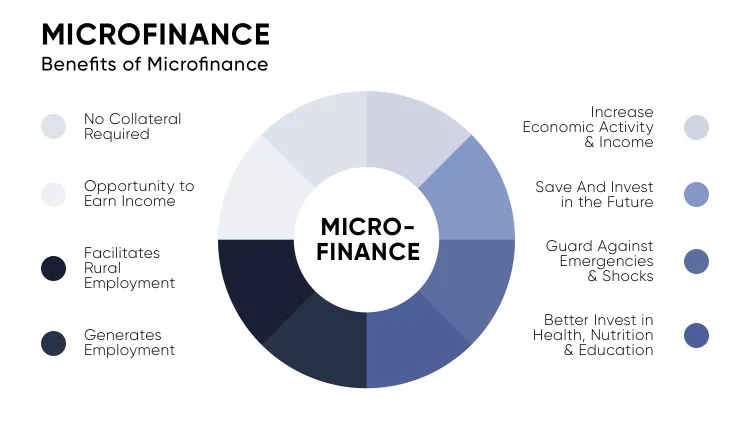

Microfinance loans: What it is, Types, and Examples

-

The Art of Luxury Interiors: A Journey into Elegance and Comfort / 4 months

- January 28, 2025

- 0

- 5 min read

A form of banking service known as microfinance, or microcredit, is given to low-income people or organizations who would not otherwise have access to financial services. Nonetheless, a lot of banks give extra services including checking and savings accounts, and some could also offer microinsurance products and business and financial education. In this blog, we will dive into microfinance bank loans, its types and examples.

Microfinance Loans: What Are They?

People with little to no regular income might obtain funding to meet their financial needs with the aid of microfinance loans. For people who are ineligible to apply for traditional loan options with more stringent requirements, several alternatives have been created.

Both personal and company financial obligations can be satisfied with microloans. It allows people with low incomes to live independently while also assisting start-ups with limited resources in raising finance. These people or groups of individuals might have their requirements examined by microfinance institutions (MFIs), who then provide the necessary financial support.

One type of loan that particularly meets the needs of those with disadvantaged wages and those from lower-income groups is microfinance loans. These loans have quite high administrative fees. In order to pay for these short-term loans’ administrative expenses, the lenders raise interest rates.

These microcredit choices encourage entrepreneurship and contribute to a population that is financially stable throughout the region in which it works. Microfinance institutions are the organizations that provide these loans.

How Do Loans for Microfinance Operate?

Microfinance loans are intended for people who are ineligible for conventional financing choices or who are unable to obtain other loan options because of more stringent eligibility requirements. People from low-income groups or with little income can create savings accounts, take advantage of fund transfers, obtain microcredit facilities, and more thanks to microfinance.

In 1976, Bangladeshi economist Muhammad Yunus created microfinance because he believed it would help the society’s economically disadvantaged members achieve financial independence. Furthermore, these loans are used by start-ups as working capital loans, even though individuals obtain them to meet their needs.

Originally, the MFIs that provided these loans were non-profit institutions. However, continuing as a non-profit endeavor barely succeeded, making it impossible for them to survive, given the enormous need for finance in developing nations. They became for-profit companies as a result.

Microfinance loans have higher interest rates than other types of lending. This is because lending money to the economically disadvantaged segments of society entails a risk for the lenders. The greater the danger, the interest rate is greater. Additionally, these loans have significant administrative costs—roughly 10% to 15% of the total loans. Additionally, because the loans are granted for a very little period of time, the banks attempt to offset the administrative expenses by raising interest rates.

Inflation and currency fluctuations are also the main reasons why financial institutions experience losses. As a result, they preserve the bare minimum of operating profits—roughly 5–10% margin—for themselves. Therefore, inflation and currency fluctuations don’t make their losses bigger. Nonetheless, they have a major impact on the microcredit alternatives’ interest rates.

Types

These loans are classified into two categories of microfinance loans based on two models. A relationship-based model is the first, and a collective model comes in second. Because of the friendly terms they negotiate with the bank, the former assists small firms and entrepreneurs in getting their loans granted. Conversely, when a group of people apply for a loan together, the latter allows the services to be facilitated for them.

For instance, to better grasp the idea, let’s look at the following examples of microloans:

Example #1

Shelly intends to purchase a business unit and grow her home-based enterprise. But in order to buy a commercial unit, she needs a substantial amount of money. The lenders deemed her unfit for the traditional loan as she lacked documentation of her consistent income.

The owner applied for microcredit after learning about it. She was shocked to learn that the loan terms were sufficiently forgiving. In order to move on with establishing her first unit, she applied for the same.

Examples #2

According to a recent article, Eskala, a start-up that split out from Global Brigades, a non-profit organization, plans to use the micro-equity technique to acquire equity positions in the businesses it has invested in instead of dealing with the hassles of loans.

A few years ago, the parent business made the same effort, receiving a $98,000 World Bank grant to support economic development initiatives in rural Central America. Because of the micro-equity approach used in this work, banks were able to take minor equity holdings against the growth capital they supplied without facing any loan problems.

Bottom Line

Microfinance loans help many low-income groups become financially stable with respect to their personal and professional requirements. However, one must be aware of a few risks involved in facilitating these financing options. If you are looking for a microfinance loan, JS Bank is the place to go.