English

English

Office Clearance for SMEs: Affordable Solutions Businesses

Office Clearance for SMEs: Affordable Solutions Businesses

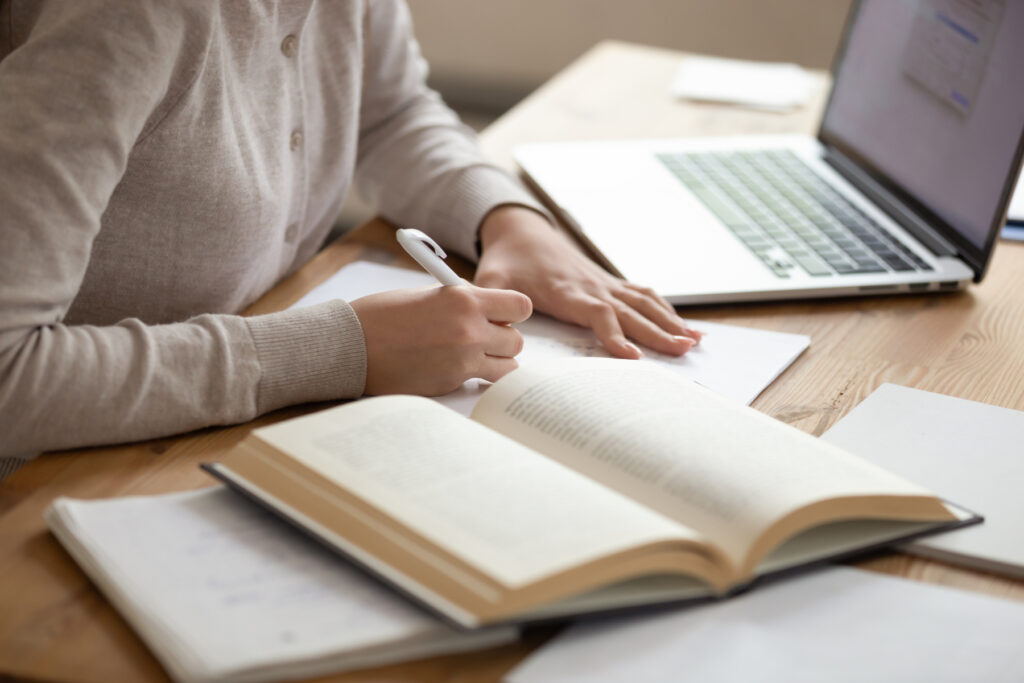

Decoding Return of Premium in Term Plans

Term plans are a fundamental component of financial planning, offering crucial protection for your loved ones in case of an unforeseen event. They provide a financial safety net, ensuring your family’s future remains secure even in your absence. While the primary purpose of a term plan is to provide a death benefit, many insurers offer an optional feature known as Return of Premium (ROP). This feature has become increasingly popular, but it’s essential to understand its nuances before making a decision.

What is Return of Premium?

Traditional term plans offer a death benefit if the insured passes away during the policy term. If the policyholder survives the term, no maturity benefit is paid. This is where ROP comes in. With the ROP option, if the insured outlives the policy term, the total premiums paid throughout the policy duration are returned. Essentially, it’s like getting your money back. This feature addresses a common concern about term plans – that nothing is received if the policyholder survives the term.

How Does ROP Work?

When you opt for a term plan with the ROP feature, you’ll typically pay a slightly higher premium compared to a standard term plan. This additional cost covers the return of premium benefit. The premiums are calculated in such a way that the insurer can return the total premium amount at the end of the policy term, assuming the insured survives. The returned amount is usually considered tax-free, adding to its appeal.

Advantages of ROP Term Plans

The most obvious advantage of an ROP term plan is the return of premiums at maturity. This can feel like a safety net within a safety net. It’s particularly attractive to those who are hesitant about the “nothing back” aspect of regular term insurance. The lump-sum amount received can be used for various purposes, such as retirement planning, children’s education, or even as a down payment for a house. Essentially, it provides a financial cushion at the end of the policy term.

Disadvantages of ROP Term Plans

While the return of premium sounds appealing, it comes at a cost. Premiums for ROP plans are significantly higher than those for standard term plans. This means you’ll be paying more throughout the policy duration. The difference in premium can be substantial, and it’s crucial to evaluate whether the return of premium justifies the extra expense. Another point to consider is that the returned amount is not adjusted for inflation. So, while you receive the total premiums paid, their actual value might be less in the future due to inflation.

Comparing ROP and Standard Term Plans

The core difference between the two lies in the maturity benefit. A standard term plan offers a lower premium but no maturity benefit. An ROP plan offers a return of premiums at maturity but at a higher premium. Choosing between the two depends on your individual financial situation and priorities. If you’re looking for the most cost-effective way to secure a death benefit, a standard term plan is generally the better option. However, if you’re comfortable paying a higher premium and value the return of premiums at maturity, an ROP plan might be suitable.

Factors to Consider When Choosing

Several factors should be considered before opting for an ROP term plan. Your age, health, financial goals, and risk appetite are crucial considerations. If you’re young and healthy, you might consider investing the difference in premium between an ROP and a standard term plan in other investment avenues. This could potentially yield higher returns over the long term. However, if you’re risk-averse and prefer a guaranteed return, even if it’s not adjusted for inflation, an ROP plan might be a good choice.

Is ROP Right for You?

The decision of whether to choose an ROP term plan or a standard term plan is a personal one. There’s no one-size-fits-all answer. It’s essential to carefully evaluate your financial situation, understand the pros and cons of each option, and choose the plan that best aligns with your needs and goals. Consider consulting with a financial advisor to get personalized advice based on your individual circumstances. They can help you assess your needs and make an informed decision about the type of term plan that’s most appropriate for you. Remember, the primary purpose of any term plan is to provide financial security for your family. Ensure you have adequate coverage, regardless of whether you choose an ROP or a standard term plan.